")

My cousin in Ohio texted me back in August, practically panicking: “Should I just buy the EV NOW before this credit thing disappears?” At the time I brushed it off a little — tax stuff always sounds more dramatic than it actually is, right? Well, turns out this one wasn’t hype. The federal EV tax credits really did end, and now that we’re well into 2026, I’ve had a bunch of friends and readers asking me the same basic question: “Okay, so what does this actually change for someone like me?”

I spent a weekend digging through this — not just reading headlines, but actually working out what it means in dollar terms for different types of buyers. Here’s what I found.

What actually happened

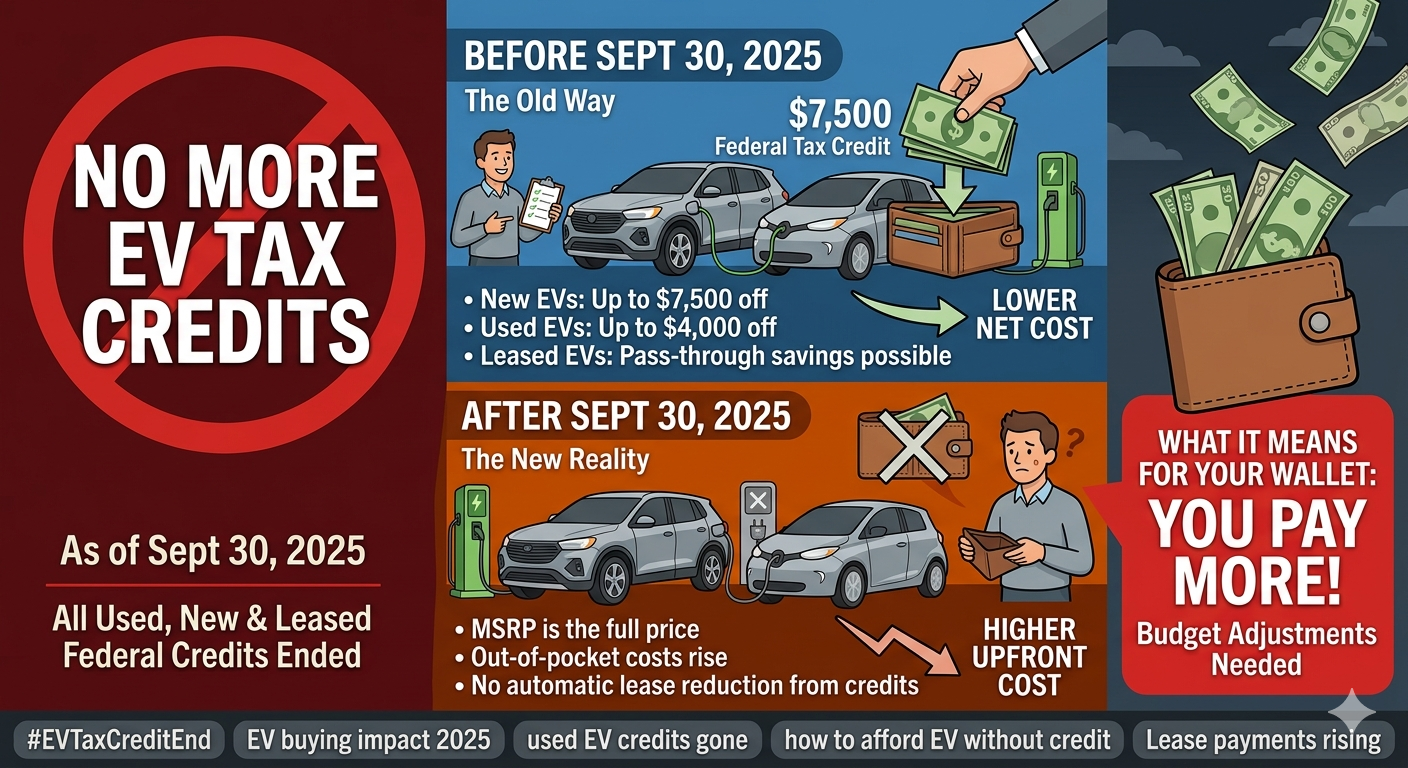

As part of the tax legislation passed in July 2025, the federal EV tax credit worth up to $7,500 for new EVs and $4,000 for used EVs officially ended on September 30, 2025. This wasn’t a slow phase-out like some previous changes — it was a hard stop with no warning beyond that final deadline, even though the credits were originally supposed to run through 2032.

So if you bought or took delivery of an EV before that date, you might still be able to claim the credit on your taxes. But if your purchase happened after September 30, 2025 — that credit is just gone. No phase-down, no partial amount, nothing.

There’s one extra wrinkle worth knowing about home chargers too. The separate tax credit for home EV charger installation (the Alternative Fuel Refueling Property credit) is set to end after June 30, 2026, so if you’re planning a home charging setup, that’s a deadline worth keeping on your radar.

Why this matters more than people think

Here’s the part that actually surprised me when I crunched the numbers. The average new EV cost around $57,245 as of August 2025, and that $7,500 credit represented roughly a 13% discount on that price. That’s not a rounding error — that’s real money. For a lot of middle-income buyers, that credit was the difference between an EV being “comparable” to a gas car and being noticeably more expensive.

I also noticed something interesting when I looked at sales data — EV sales actually surged almost 18% year-over-year in August 2025, right as everyone rushed to beat the deadline. That tells you something: a LOT of people were waiting on the fence, and that credit was the nudge that got them to commit.

What this means depending on your situation

I broke this down into a few scenarios because “what does this mean for your wallet” really depends on where you are in the buying process.

If you already bought before September 30, 2025: You’re probably fine — you can likely still claim it. But don’t assume it’s automatic. You claim the credit when filing your federal income taxes using Form 8936, and it’s a non-refundable credit, meaning it can only reduce your tax liability to zero — it won’t generate a refund beyond what you owe. So if your tax bill for the year is smaller than $7,500, you won’t get the full benefit. This trips people up more than you’d expect.

If you’re buying now, in 2026: The credit simply isn’t there anymore for most standard purchases. There’s a narrow exception — leased EVs under the commercial clean vehicle program had credits that extended to December 31, 2025 for most automakers, but even that window has now closed. For the vast majority of buyers reading this in mid-2026, the federal incentive is off the table, period.

If you’re considering a used EV: Same story — the used EV credit applied to vehicles placed in service between January 1 and September 30, 2025, so that’s also done.

The part nobody’s talking about enough — state incentives

Here’s where I think people are leaving money on the table without realizing it. While the federal credit is gone, many state and local governments continue to offer their own rebates and incentives that can still make EV ownership more affordable.

This varies wildly by state — some have rebates, some have reduced registration fees, some have utility-company incentives for charging equipment. My honest advice: don’t just assume “no federal credit means no help at all.” Spend 30 minutes searching your state energy office’s website or your local utility company’s EV program page. I was surprised how many of these programs still exist and aren’t widely advertised.

What I’d actually do if I were buying an EV right now

- Don’t expect the sticker price to drop to compensate. Industry watchers expected this to be a real test for the EV market without federal support behind it, but that doesn’t mean dealers will automatically discount by $7,500 to make up the difference. Some might offer manufacturer incentives to keep sales moving, but that’s not guaranteed or consistent.

- Check state-level programs first, before you even start comparing models. This can genuinely shift your budget more than people expect.

- Recalculate your break-even point. If you were comparing EV vs. gas car costs using a calculation that assumed a $7,500 discount, redo that math without it. The ownership math (fuel/charging savings, lower maintenance) still holds — it just takes longer to “pay off” the price difference now.

- If you’re leasing, ask directly whether any manufacturer-specific incentives are baked into the lease deal. Some manufacturers have started offering their own incentives to soften the blow of the federal credit disappearing, separate from any government program.

- Don’t panic-buy. I know that sounds obvious, but a few people I talked to felt like they’d “missed the boat” and were second-guessing decisions they’d already made. The credit ending doesn’t mean EVs stopped making financial sense — it just means the math is a little less favorable than it was a year ago. Run your own numbers (purchase price, charging costs vs. fuel, maintenance) rather than basing the decision purely on whether a credit exists.

The honest bottom line

If you were counting on that $7,500 (or $4,000 for used) to make an EV purchase work financially, you need to redo your budget — that money isn’t coming from the federal government anymore, full stop.

But it’s not the end of the EV math story. Electricity costs, lower maintenance, and any state-level programs you can find are still real savings that exist independently of this change. The decision just requires a bit more homework than it did a year ago, and honestly, that’s not a bad thing — it forces you to look at the actual total cost rather than relying on a credit to paper over the gap.

If you’re on the fence right now, my suggestion is simple: don’t make this decision based on what the tax credit used to be. Make it based on what your actual numbers look like today, in 2026, with the rules as they currently stand.